How Readiness 2030 Revived Defence Investment

The End of the Peace Dividend?

For more than three decades after the end of the Cold War, Europe benefited from what became known as the “peace dividend”. With the Soviet threat receding, governments across the continent reduced defence spending and redirected resources toward domestic priorities. Defence budgets shrank, procurement cycles slowed, and industrial capacity contracted. This was not a short‑term adjustment but a generational shift in how Europe viewed its security environment. There was an assumption that large‑scale conflict on or near the continent was unlikely.

That era ended abruptly in 2022. Russia’s invasion of Ukraine fundamentally reshaped Europe’s security outlook, forcing governments to rebuild military readiness and industrial capacity at a pace not seen in a generation. Fundamental gaps in stockpiles, production capacity, and technological readiness were exposed. It also demonstrated that modern warfare requires sustained industrial output, rapid innovation cycles, and resilient supply chains. For Europe, this was a catalyst for reassessing and reviving its military readiness.

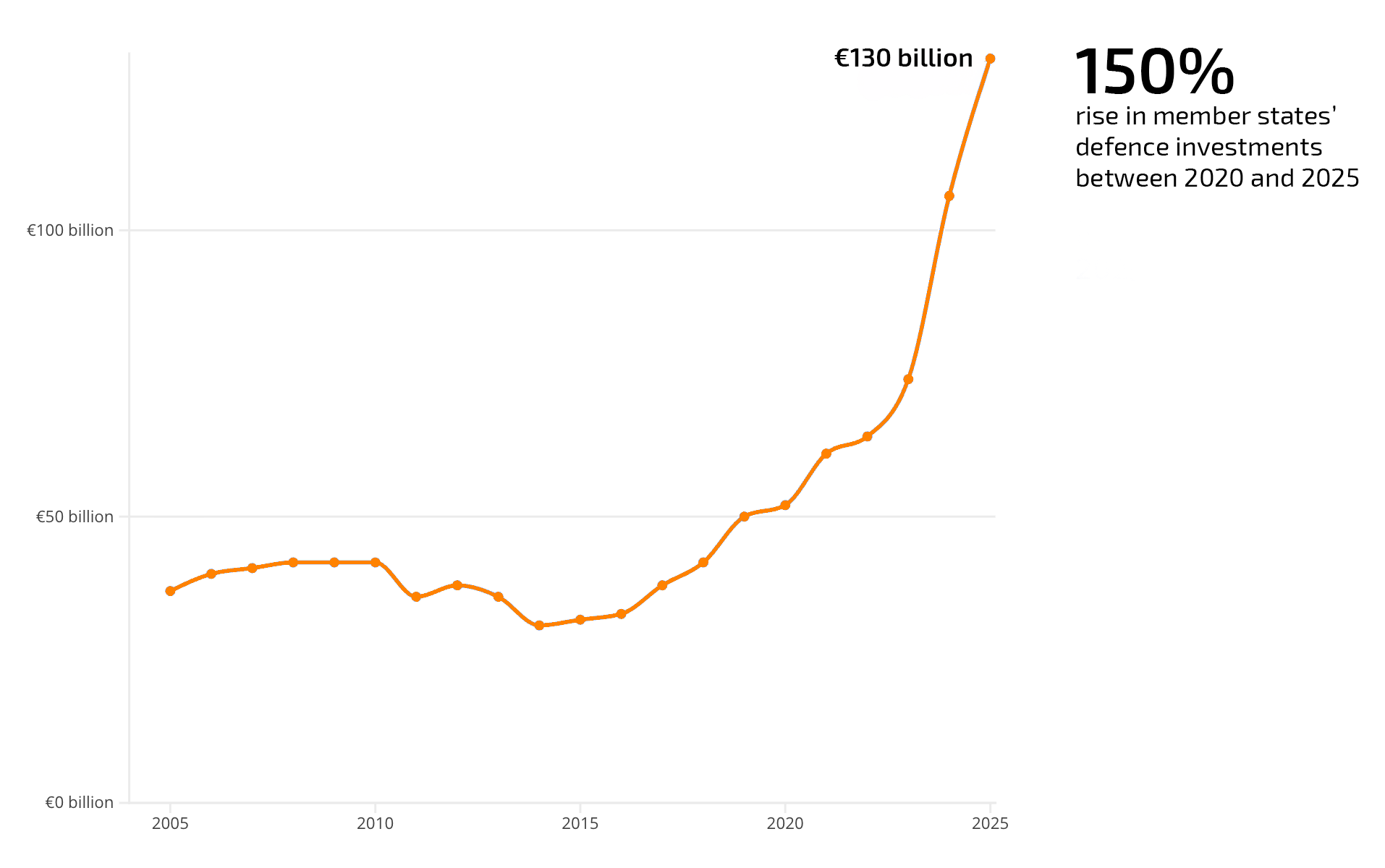

The shift is visible in the numbers. Between 2020 and 2025, defence investment increased by roughly 150 percent. Global defence spending has experienced its steepest rise since the end of the Cold War, with virtually every European nation increasing their military spending in 2024.

Defence investments (2005-2025). Source: European Defence Agency

This new investment trajectory was formalised in March 2025 with the European Commission’s ReArm Europe Plan/Readiness 2030 initiative. Quickly rebranded to Readiness 2030 following concerns the name was overly militaristic, it aims to modernise Europe's defence capabilities and mobilise up to €800 billion on defence investment by 2030[1]. Readiness 2030 is centred around three key themes:

increased defence spending to close long‑standing readiness gaps;

deliberate strengthening of sovereign industrial capability so it can produce and sustain critical technologies domestically; and

sustained support for Ukraine, whose experience has become both a catalyst and a warning for policymakers.

Rising Defence Spending Across the Continent

The first major force reshaping Europe’s defence environment is the structural recalibration and sustained increase in defence spending. The political consensus behind this is broad and durable, spanning governments of different ideological backgrounds, with a shared recognition of the fundamental need that Europe must rebuild its readiness, replenish depleted stockpiles, and modernise its forces to meet contemporary threats.

Germany illustrates the scale of the change. Despite being Europe’s largest economy, it has historically maintained a modest defence industrial footprint. Spending has doubled since 2022 and is projected to reach 3.5 percent of GDP by 2030, which is an almost fourfold increase in eight years. Germany’s Zeitenwende, or “turning point”, is not merely a political slogan but a multi‑year approach to reshape procurement priorities and accelerate acquisition timelines. Procurement processes that once moved slowly are now demanding proven, interoperable and ready-to-deploy capabilities.

Other major European economies are undergoing similar transitions. France is accelerating its defence spending to reach €64 billion in 2027, three years earlier than planned and double 2017 defence spending [2]. Poland has embarked on one of the most ambitious modernisation programs, driven by its proximity to the conflict and its strategic role on NATO’s eastern flank. Spending more than 4 percent of GDP on defence, the highest proportion in NATO, Poland is prioritising investment in autonomous and AI-supported systems to improve the effectiveness of their military personnel [3].

As militaries modernise and the nature of warfare evolves, defence technologies such as counter-drone are of increasing demand. Counter-drone and electronic warfare solutions (including embedded AI) are now central elements of modern defence planning. For DroneShield, this environment aligns directly with the company’s core capabilities in the detection and defeat of drones through its array of hardware and software solutions, and is evidenced by 45 per cent of 2025 revenues coming from Europe.

Europe’s Push for Sovereign Industrial Capability

A key theme throughout Readiness 2030 is the drive for sovereign industrial capability. This means an ability to design, manufacture and sustain critical defence technologies at accelerated lead times and short turn-around delivery capabilities. The shift is not only about capability but also about resilience. European nations want supply chains that are predictable, secure, and geographically anchored within the continent.

In meeting the priority demand for counter-drone solutions, DroneShield’s expansion in Europe is aligned with this environment. In March 2026, the company's European Headquarters was officially opened in Amsterdam, and its EU manufacturing capability was announced. The establishment of localised C-UAS manufacturing responds to increased momentum for mature, scalable, and sovereign capability. As part of this collaboration, DroneShield has established and will continue to grow a primarily EU-based supply chain, positioning the company more competitively for EU procurement opportunities.

Image: DroneShield officially opens its European Headquarters

The importance of sovereign capability also reflects fresh lessons which are front of mind from recent conflicts. Ukraine demonstrates that industrial capacity is just as important as battlefield capability. Nations that cannot produce or replenish critical systems quickly face significant operational challenges. A reweighting in the alliances between the United States and Europe has pushed Europe to rebuild its industrial base, expand production lines, and encourage companies to localise manufacturing. DroneShield’s decision to establish a European manufacturing capability aligns directly with this trend and positions the company to participate in long‑term procurement programs that prioritise European industrial manufacturing.

European Support for Ukraine

Supporting Ukraine is central to Europe’s security strategy. Alongside diplomatic engagement and substantial military assistance, by enabling Kyiv to defend itself, Europe reinforces its own security and sends a clear signal regarding territorial aggression. European support to the nation has never been more vital, with the military aid allocation to Ukraine rising by 67 per cent in 2025.

Support for Ukraine has become a matter of both sovereignty and political necessity for European nations. Russia’s illegal invasion posed a direct threat to European security, forcing neighbouring states to recognise that Ukraine’s defence is inseparable from their own stability. DroneShield has been proud to support Ukraine efforts from the beginning. As a pioneer in the counter-drone market, DroneShield recognised the impact drones could have on modern warfare. Today, hundreds of DroneShield detection and defeat products are deployed in Ukraine. Feedback from the field has provided many harrowing examples where DroneShield’s CUAS solutions have saved lives in Ukraine.

What Readiness 2030 means for Investors

Readiness 2030 marks the most significant shift in European defence policy and spending in a generation. After decades of under investment, governments are now committing to long term increases in defence budgets. They are rebuilding stockpiles and accelerating procurement cycles. This is not a temporary response to a single conflict. It is a durable reorientation of European security strategy that prioritises readiness, industrial resilience, and sustained support for Ukraine.

For industry, the implications are profound. Defence ministries want technologies that can be produced at scale, updated rapidly, and supported locally. Sovereign industrial capability is now a central procurement requirement. Companies with European manufacturing and supply chains are increasingly advantaged. At the same time, the rapid evolution of drone warfare has made counter‑drone and electronic warfare essential to modern defence planning.

DroneShield sits at the intersection of these trends. The company has a growing European footprint and proven operational performance. Its product suite aligns with emerging capability priorities. DroneShield is well placed to benefit from Europe’s long term rearmament cycle. For investors, Readiness 2030 represents a multi-year growth opportunity in a rapidly expanding market.

References

[1] Cassandra Tanti, “EU defence initiative rebranded as ‘Readiness 2030’ after backlash from Italy and Spain,” Monaco Life, 24 March 2025.

[2] Rudy Ruitenberg, “France to quicken defense-spending boost in bid to be ‘feared’,” Defense News, July 14, 2025.

[3] Darius von Guttner, “Poland’s mass‑army turn is reshaping NATO’s eastern flank,” The Strategist (ASPI), 9 February 2026.